The end of London Interbank Offered Rates (LIBOR) is no surprise to most people working in the banking industry. The migration to Alternative Reference Rates (ARR) has been underway for several years, gaining momentum in 2017 when UK regulators withdrew their support for the LIBOR benchmark setting process. Even the outbreak of COVID-19 and the unsettled status of Brexit negotiations have not moved the 2021 year-end date of LIBOR’s cessation. Currently, there are in excess of $5 Trillion in US business and consumer loans outstanding that rely on LIBOR benchmarks.[i] Every single lending agreement underlying these exposures will need to be remediated prior to the LIBOR end date. Many of these loans will require individual discussion and modification with borrowers. The largest US banks have tens of thousands of lending agreements that are subject to modifications, which will require significant time and resources. For a single agreement, negotiations with borrowers and legal representatives can take months. Creating a framework that balances the inherent complexities of moving to a new benchmark rate, client interests and preferences, and banks’ resource constraints is a delicate task.

Creating a Pathway to Consent

Renegotiating client agreements on a large scale is not a new activity for US banks. In recent years banks have already had to modify a vast proportion of their derivatives agreements to adhere to the QFC US Stay protocol. Moving clients from LIBOR to ARR benchmarks is more challenging because in many instances, explicit client consent is required to enact the changes. The benchmark migration process involves several steps, including identification of all exposures that rely on LIBOR benchmarks, initial client outreach to explain the need for the intended change, contract negotiations, document drafting and approval, and finally rebooking of the loan. This process can be complex and time consuming and it is therefore essential that banks find efficient methods to obtain client consent without breaching trust that might jeopardize the ongoing business relationship.

One Goal, Many Options

Legacy loan agreements generally fall into one of the four categories as shown in Figure 1 below. Client discussions for contracts where the LIBOR successor rate is pre-determined (Disclosure Only), or where banks have the right to choose a new benchmark rate (Coordinate), are generally straightforward. However, it is critical that the rationale for changing the base rate and potential implications of that change are fully explained to all impacted clients. Failure to do so on a consistent basis triggers significant legal risks if clients feel that banks are not acting in the client’s best interests.

Figure 1 : Transition Options

By contrast, client negotiations for loan agreements where no replacement rate is identified (Silent), or where the successor benchmark is subject to bi-lateral negotiation, are much more complex. Both parties must agree to all proposed changes and banks need to ensure that their clients understand that adherence to LIBOR benchmarks is not a sustainable option. This multi-step negotiation process can take up to three months, and potentially longer for syndicated credit agreements that require consensus from a larger stakeholder group.

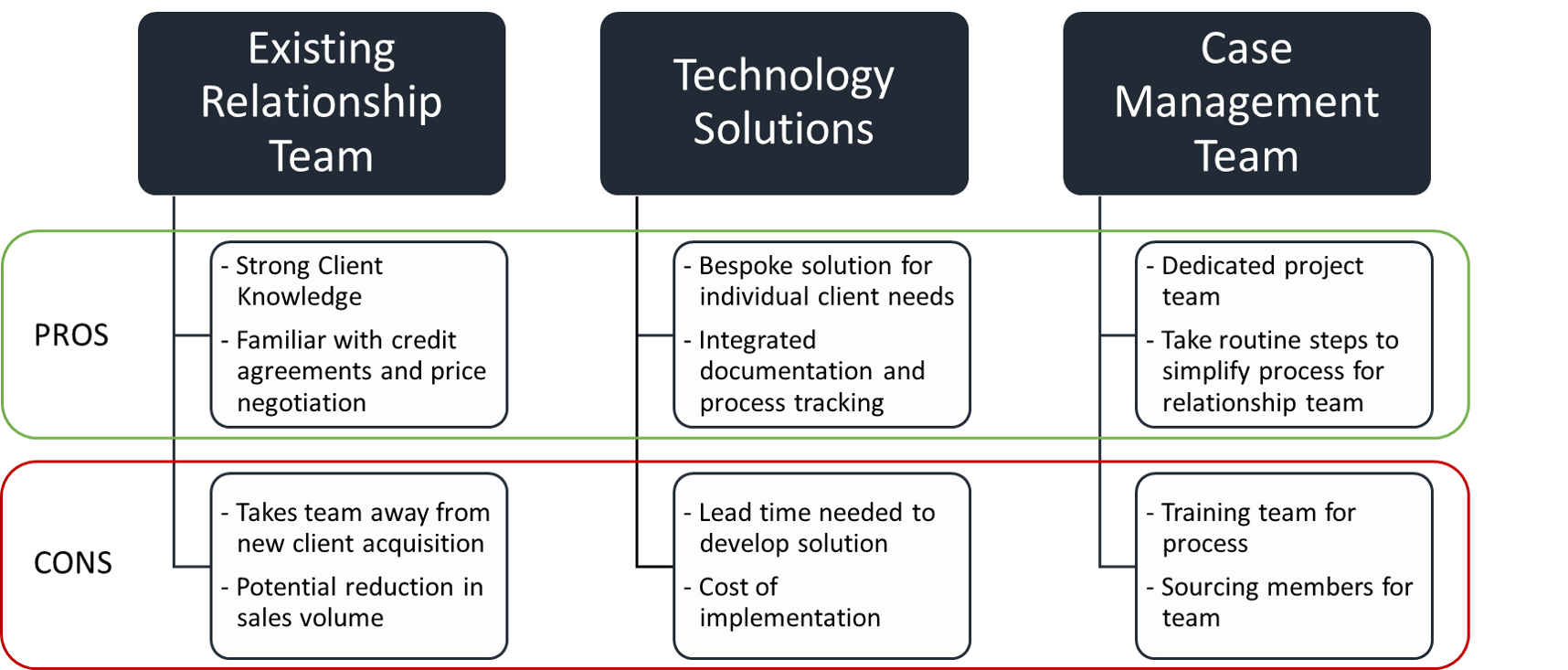

The Case for Case Managers

Banks have several options to tackle the volume of contract negotiations. In many situations, banks will want to leverage their existing relationship teams. Client relationship managers know their clients’ individual financial objectives, negotiation styles and personal preferences. Many banks augment their relationship teams with technology solutions to centralize status updates, standardize documentation processes, and record client communications. Several larger banks have established a dedicated Case Management team that assists relationship managers with the minutia of the negotiation process. A Case Management team allows the relationship team to remain informed of the negotiation status for key clients without distracting them from their usual business development tasks. To identify the best solution, individual banks need to assess available options considering resourcing, cost and client relationship impacts as outlined in Figure 2 below.

Figure 2: Process, Technology and People Solutions

Program Deliverable Challenges

When assessing potential client negotiation strategies, it is important to balance the overall objectives of the LIBOR transition program and contrast those with the key focus areas of the various component solutions. Viewed in isolation, none of the proposed client outreach strategies fulfill typical LIBOR transition goals such as client retention and management, ongoing profitability, and risk management. Banks need to tailor their approaches based on their individual client and exposure profiles. Based on our experience assisting large banks in structuring their client outreach strategies, a holistic approach that combines all of the three component solutions yields the most promising results. Combining the approaches enables the bank to efficiently manage the incremental work required during the LIBOR migration and ensure that the clients are migrated fairly and in a manner consistent with the bank’s philosophy.

About Monticello

Monticello consultants have extensive experience in the implementation of large-scale regulatory initiatives. Our firm understands the importance of diligent analysis, program management, and collaboration across teams within major financial institutions and across the industry. Our current work on LIBOR Transition, Uncleared Margin Rules (UMR), Qualified Financial Contract (QFC) Record Keeping and US Stay regulations demonstrates the important regulatory expertise our consultants bring to our clients. Our teams possess deep knowledge of capital markets instruments, legal agreements and operational processes, as well as the related data and information systems impacts that will be in focus for the migration to RFRs. Monticello teams are dynamic, flexible, and highly motivated to assist you in your transition to a post-LIBOR future.

[i] Alternative Reference Rates Committee : SOFR Starter Kit Part I , Alternative Reference Rate Committee, www.newyorkfed.org/medialibrary/Microsites/arrc/files/2020/ARRC_Factsheet_1.pdf.